Qlib: Quantitative Platform¶

Introduction¶

Qlib is an AI-oriented quantitative investment platform, which aims to realize the potential, empower the research, and create the value of AI technologies in quantitative investment.

With Qlib, users can easily try their ideas to create better Quant investment strategies.

Framework¶

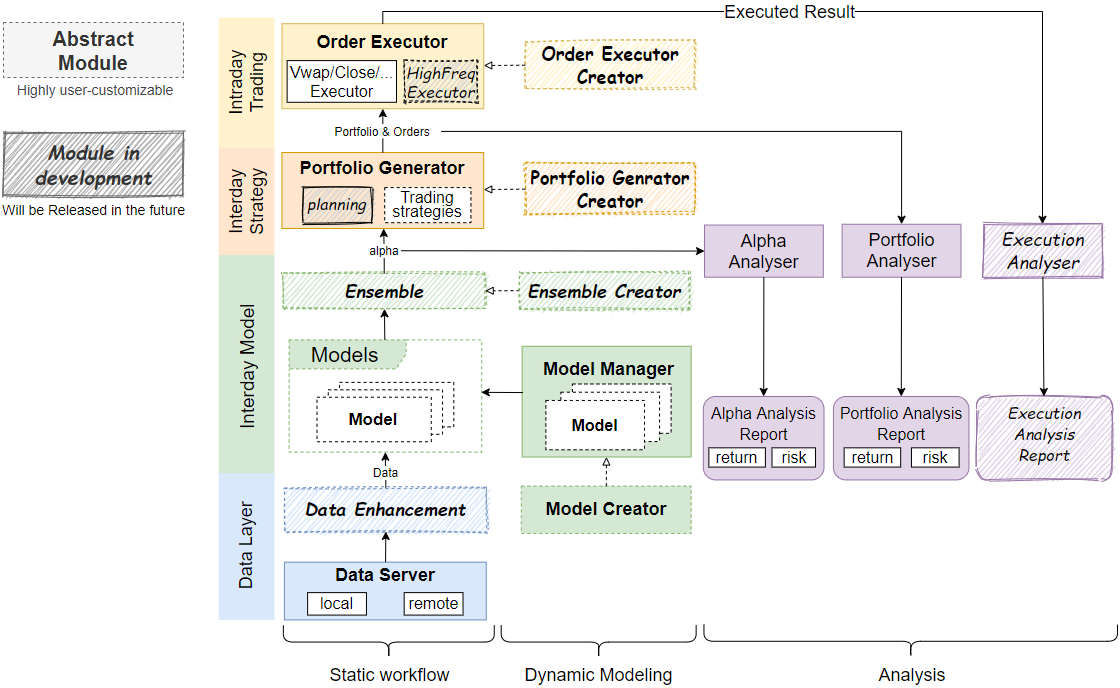

At the module level, Qlib is a platform that consists of above components. The components are designed as loose-coupled modules and each component could be used stand-alone.

| Name | Description |

|---|---|

| Data layer | DataServer focuses on providing high-performance infrastructure for users to manage and retrieve raw data. DataEnhancement will preprocess the data and provide the best dataset to be fed into the models. |

| Interday Model | Interday model focuses on producing prediction scores (aka. alpha). Models are trained by Model Creator and managed by Model Manager. Users could choose one or multiple models for prediction. Multiple models could be combined with Ensemble module. |

| Interday Strategy | Portfolio Generator will take prediction scores as input and output the orders based on the current position to achieve the target portfolio. |

| Intraday Trading | Order Executor is responsible for executing orders output by Interday Strategy and returning the executed results. |

| Analysis | Users could get a detailed analysis report of forecasting signals and portfolios in this part. |

- The modules with hand-drawn style are under development and will be released in the future.

- The modules with dashed borders are highly user-customizable and extendible.