Portfolio Strategy: Portfolio Management¶

Introduction¶

Portfolio Strategy is designed to adopt different portfolio strategies, which means that users can adopt different algorithms to generate investment portfolios based on the prediction scores of the Forecast Model. Users can use the Portfolio Strategy in an automatic workflow by Workflow module, please refer to Workflow: Workflow Management.

Because the components in Qlib are designed in a loosely-coupled way, Portfolio Strategy can be used as an independent module also.

Qlib provides several implemented portfolio strategies. Also, Qlib supports custom strategy, users can customize strategies according to their own needs.

Base Class & Interface¶

BaseStrategy¶

Qlib provides a base class qlib.contrib.strategy.BaseStrategy. All strategy classes need to inherit the base class and implement its interface.

- get_risk_degree

- Return the proportion of your total value you will use in investment. Dynamically risk_degree will result in Market timing.

- generate_order_list

- Return the order list.

Users can inherit BaseStrategy to customize their strategy class.

WeightStrategyBase¶

Qlib also provides a class qlib.contrib.strategy.WeightStrategyBase that is a subclass of BaseStrategy.

WeightStrategyBase only focuses on the target positions, and automatically generates an order list based on positions. It provides the generate_target_weight_position interface.

- generate_target_weight_position

- According to the current position and trading date to generate the target position. The cash is not considered in the output weight distribution.

- Return the target position.

Note

Here the target position means the target percentage of total assets.

WeightStrategyBase implements the interface generate_order_list, whose processions is as follows.

- Call generate_target_weight_position method to generate the target position.

- Generate the target amount of stocks from the target position.

- Generate the order list from the target amount

Users can inherit WeightStrategyBase and implement the interface generate_target_weight_position to customize their strategy class, which only focuses on the target positions.

Implemented Strategy¶

Qlib provides a implemented strategy classes named TopkDropoutStrategy.

TopkDropoutStrategy¶

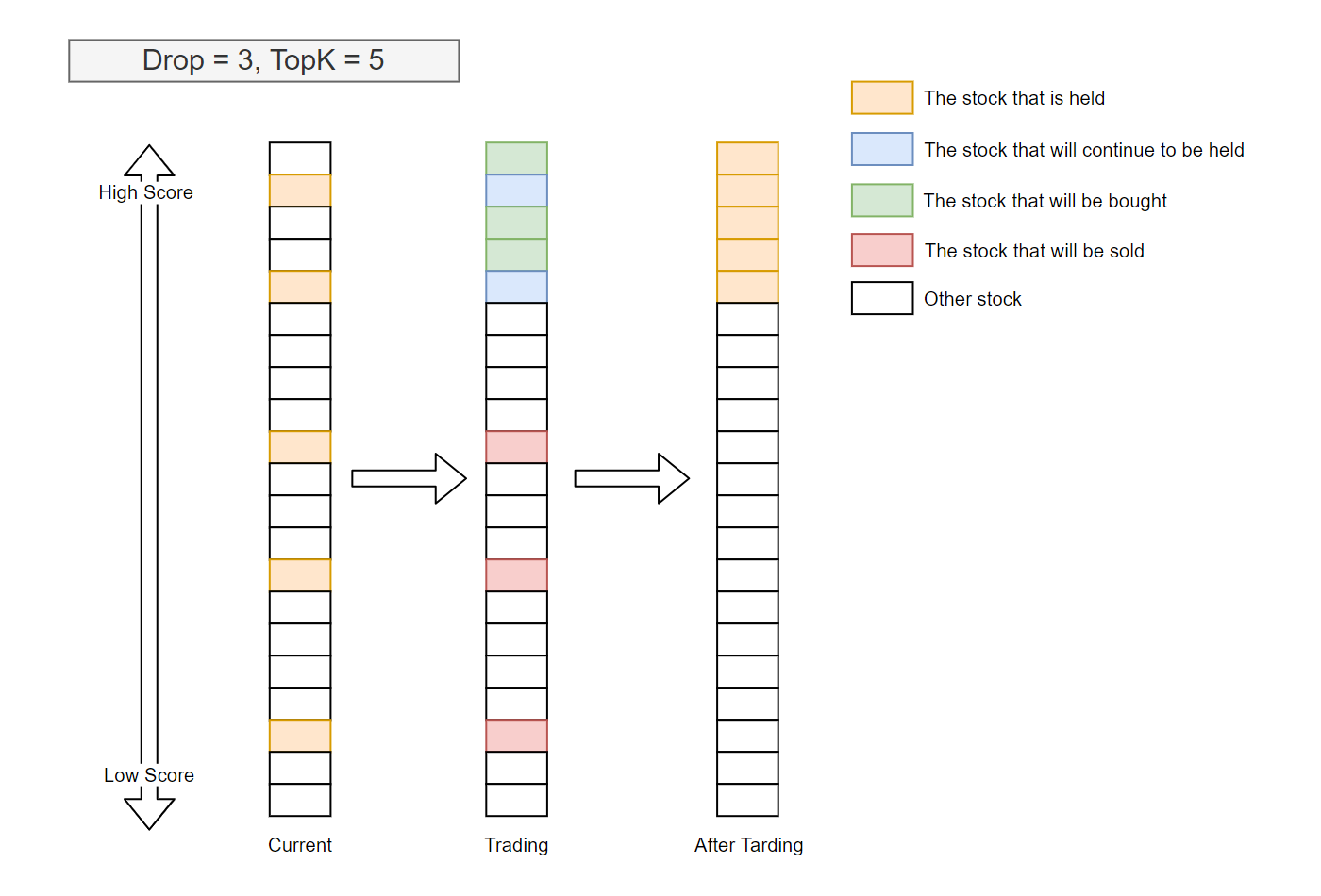

TopkDropoutStrategy is a subclass of BaseStrategy and implement the interface generate_order_list whose process is as follows.

Adopt the

Topk-Dropalgorithm to calculate the target amount of each stockNote

Topk-Dropalgorithm:- Topk: The number of stocks held

- Drop: The number of stocks sold on each trading day

Currently, the number of held stocks is Topk. On each trading day, the Drop number of held stocks with the worst prediction score will be sold, and the same number of unheld stocks with the best prediction score will be bought.

TopkDropalgorithm sells Drop stocks every trading day, which guarantees a fixed turnover rate.Generate the order list from the target amount

Usage & Example¶

Portfolio Strategy can be specified in the Intraday Trading(Backtest), the example is as follows.

from qlib.contrib.strategy.strategy import TopkDropoutStrategy

from qlib.contrib.evaluate import backtest

STRATEGY_CONFIG = {

"topk": 50,

"n_drop": 5,

}

BACKTEST_CONFIG = {

"verbose": False,

"limit_threshold": 0.095,

"account": 100000000,

"benchmark": BENCHMARK,

"deal_price": "close",

"open_cost": 0.0005,

"close_cost": 0.0015,

"min_cost": 5,

}

# use default strategy

strategy = TopkDropoutStrategy(**STRATEGY_CONFIG)

# pred_score is the `prediction score` output by Model

report_normal, positions_normal = backtest(

pred_score, strategy=strategy, **BACKTEST_CONFIG

)

Also, the above example has been given in examples/train_backtest_analyze.ipynb.

To know more about the prediction score pred_score output by Forecast Model, please refer to Forecast Model: Model Training & Prediction.

To know more about Intraday Trading, please refer to Intraday Trading: Model&Strategy Testing.

Reference¶

To know more about Portfolio Strategy, please refer to Strategy API.